BancAlliance Navigating the Economic Clouds Ahead

As many of our members are keenly aware, the prediction of an oncoming recession grows louder by the day. In our view, there are two likely macro paths that could potentially impact various portions of the BancAlliance portfolio. The first is that the Federal Reserve overcorrects on interest rates and forces an economic slowdown. The second is that inflation continues to remain elevated, but the economy continues to grow, albeit at a slower pace.

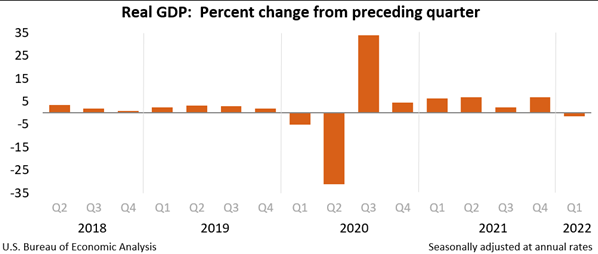

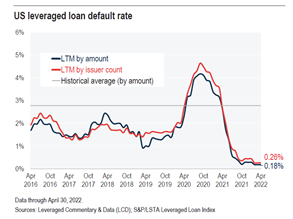

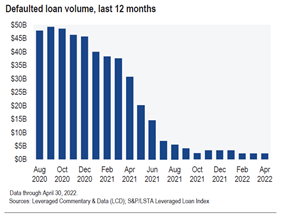

The difficulty of a forecasting exercise is that a recession is a lagging indicator, defined as two successive quarters of negative GDP Growth. Thus far, by that metric we have yet to qualify as being in a recession and the leveraged loan market has continued in a historical low default environment.

After segmenting and reviewing the BancAlliance (“BA”) portfolio in detail, Alliance Partners (“AP”) has yet to see any deterioration of the portfolio as a whole or within a specific industry. Furthermore, the borrowers currently on the AP/BA watchlist (loans rated 7 or below) are there for idiosyncratic reasons as opposed to macro or systemic reasons.

Past recessions have given insight into how particular segments of the economy behave, there are certain industries that we believe may be impacted by the two scenarios above and could experience volatility in the near-term. Generally, these include cyclical industries with long purchasing cycles, volatile input costs, significant fixed cost structures and reliance on customers making large discretionary purchases. Additionally, higher fuel and input costs could potentially create added stress to certain industries. Examples of industries that may be impacted include:

- Automotive

- Heavy Manufacturing

- Chemicals

- Packaging

- Capital Equipment

- Transportation

- Certain areas of Financial Services tied to long-term fixed rates (i.e. Mortgage lenders)

It should be noted that not all industries should be painted with a broad brush, and companies have various tools at their discretion to help mitigate risks. Such tools include hedging contracts, long-dated contracts with customers that include price escalators and ability to reduce variable costs quickly. Both the basic tenets of Finance 101 and the analysis presented at BancAlliance Member Meetings heavily stress the importance of portfolio diversification. Diversification not only includes portfolio construction across different asset classes (i.e. C&I vs. Real Estate), but also requires dispersion across different industries. Diversification strives to smooth out unsystematic risk events in a portfolio, so the positive performance of some investments neutralizes the negative performance of others. The benefits of diversification hold only if the securities in the portfolio are not perfectly correlated—that is, they respond differently, often in opposing ways, to market influences[1].

The benefit of BancAlliance to our member banks is to provide the opportunity to cost-effectively diversify their balance sheets across multiple fronts relative to their core offering in their local markets.

- Geography

- Borrower Size

- Asset class (C&I)

- Rate (floating rate)

- Tenor (short term)

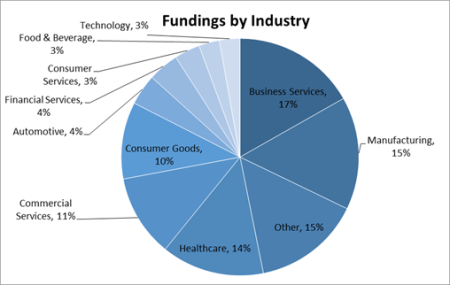

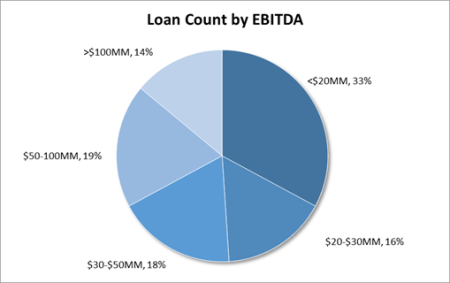

AP stresses the importance of taking granular bite sizes and taking a broad portfolio position as part of well-diversified investment strategy. Below is a snapshot of the BA portfolio based on industry and EBITDA size.

AP continues to take the following steps to maintain appropriate levels of portfolio management:

- Trough Risk Rating: If AP receives a forecast indicating future deterioration in financial performance, AP will risk rate off the trough or low-point of the forecast to ensure adequate and timely focus.

- Risk Rating Overrides: AP will proactively override quantitative risk rating calculations if there is information not reflected in performance. As with the initial phases of Covid-19, AP was quick to downgrade potentially impacted Borrowers and patient to upgrade based on sustained recovery.

- Agency Ratings: AP in in the process of subscribing to Moody’s/S&P reports and will post those to the portal (where applicable) for additional data points.

- Valuation: AP updates the comparable public company analysis as part of the Update Memorandum and Modification Memorandum process. As the equity markets are experiencing volatility AP will assess if the valuation multiple used in its analysis is appropriate.

- Impairment Analysis: AP runs its own impairment analysis for loans on the AP/BA watchlist. While not posted to the portal or meant to be accounting advice, we can provide to members upon request.

- Secondary Market Trading: In loans where a recovery will be long dated, AP continues to look to the secondary market for a potential exit in order to maximize recovery.

In addition to standard areas of due diligence, AP continues to focus on the following aspects during underwriting:

- Interest Rate Sensitivity: AP typically stresses an increase in base rate of over 300 bps over the life of the loan.

- Supply Chain Dynamics: A key focus of diligence is supply chain and procurement of product. This includes items such as geography and geographical diversification, underlying cost, purchase terms and availability.

- Recession Impact: Where appropriate, AP will consider a recession case in the downside scenario and sensitize the model accordingly.

- Portfolio Reports: AP is currently working creating member portfolio reports that will demonstrate the distribution of industries within each member’s portfolio and serve as a basis to consider exploring additional industries to support a balanced portfolio.

- Repayment Capacity: AP assesses repayment capacity as part of the underwriting process to ensure that the Borrower Company has the ability to generate sufficient earnings or cash to de-lever to a sustainable level and could repay total debt over a reasonable period (which AP defines as a five-to-seven-year period). It should be noted that repayment capacity analysis can only be reasonably done when a medium to long-term forecast is provided by management. For portfolio monitoring, it should be noted that BA’s risk rating matrix is highly correlated with repayment capacity as it takes into account leverage, margins, LTV and fixed charge coverage as inputs, which are driven by the same variables of repayment capacity: free cash flow and debt.

While it is still too early to call when, if or how hard a recession may impact the broader economy, AP continues to be vigilant for any signs of stress in the portfolio or overall market.

[1]https://www.investopedia.com/terms/d/diversification.asp#:~:text=Diversification%20is%20a%20risk%20management,any%20single%20asset%20or%20risk.