Recent Coverage of Growth in Leveraged Lending Market

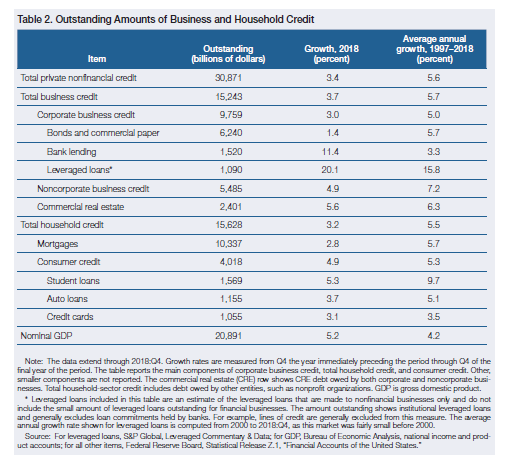

Strong growth in the leveraged lending market has been addressed recently both by Regulators and the press. The May 2019 Federal Reserve Financial Stability Report [1] (the “Report”) highlights that Leveraged Loans have grown 20.1% since 2018 and have an average annual growth rate of 15.8% from 1997 – 2018.

On May 20th, the Wall Street Journal published an article titled “Fed’s Powell Warns of Economic Risks From Rising Business Debt”.

While the headline certainly merits scrutiny, the article itself notes:

“At the same time, Mr. Powell pushed back against some of the more alarmist views about corporate borrowing, calling some comparisons to the subprime-mortgage crisis “not fully convincing.” Mr. Powell said the financial system today “appears strong enough to handle potential business-sector losses, which was manifestly not the case a decade ago with subprime mortgages.” Moreover, the increase in business debt reflects a steady “upward plod” over a long expansion, he said, as opposed to the spike in mortgage lending between 2004 and 2006.”

In addition, the Vice Chair for Supervision, Randal Quarles, recently tempered concerns about the growth in leveraged lending.

“In a talk at Yale University on Tuesday, Fed Vice Chair for Supervision Randal Quarles added the media has been overplaying and oversimplifying the story in such a way to make it seem it was analogous to “the Earth must be getting hit by an asteroid.” In particular, Quarles said leveraged loans risk “is not really a direct analog to the subprime [mortgage] lending” that caused the financial crisis. In his discussion of leveraged loans, Quarles said that the volume of business credit is very high currently, but “hasn’t grown to a level that is inconsistent with historical precedent for this point on an expansion.”[2]

The Report itself pointed to the factors below that could impact business loans and in particular, leveraged loans. Please see the bold italics for AP’s response:

1. “After growing faster than GDP through most of the current expansion, total business-sector debt relative to GDP stands at a historically high level. That said, in 2018, total business- sector debt grew a bit below its average pace since 2013. The sizable growth in business debt over the past seven years has been characterized by large increases in risky forms of debt extended to firms with poorer credit profiles or that already had elevated levels of debt. While growth in these riskier forms of debt slowed to zero in late 2016, it has rebounded more recently, with leveraged loan net issuance more than offsetting a modest decline in issuance of high-yield and unrated bonds. Issuance of leveraged loans continued at a solid pace in the first quarter of 2019, though refinancing activity has decreased because of the somewhat elevated spreads”[3]

We do not consider this a controversial statement. The leveraged loan market has grown as more private equity firms are able to access the capital markets to finance their investment strategies. Most of the increase has been driven by the rise of Collateralized Loan Obligations (“CLOs”), which are securitized products that are held by a range of investors.

A Senior PIMCO Portfolio manager highlights how to view this growth in context in her recent article:

“The U.S. leveraged loan market has grown fairly consistently since its infancy in the early 1990s and now sits in line with its more established high yield bond sibling at just over $1 trillion. There is much focus on this growth, but it’s important to put in perspective. The investment grade (IG) bond market dwarfs them both, sitting at over $5 trillion. Mortgage-related debt remains near $10 trillion. Leveraged loans have nearly doubled (based on the J.P. Morgan Leveraged Loan Index), but loan market growth still lags a 150% increased in the IG market (which has also seen deterioration in quality/ratings).[4]

2. “Credit standards for new leveraged loans appear to have deteriorated further over the past six months. The share of newly issued large loans to corporations with high leverage—defined as those with a ratio of debt-to-EBITDA (earnings before interest, taxes, depreciation, and amortization) above 6—increased in the second half of last year and the first quarter of this year and now exceeds previous peak levels observed in 2007 and 2014, when underwriting quality was poor. This apparent deterioration in credit standards notwithstanding, the credit performance of leveraged loans has remained solid, in part reflecting the relatively strong economy. The default rate on leveraged loans edged down in the most recent data to a level near the low end of its historical range.”[5]

The Report did not stratify the leveraged lending market into different categorizations (i.e. Broadly Syndicated vs. Middle Market) but instead looked at leveraged lending it in its entirety.

The Report does not quantify exactly how credit standards have deteriorated besides merely highlighting that overall leverage has increased. We have a few observations related to this point. First, BancAlliance (“BA”) has set the Risk Acceptance Criteria (RAC) policy threshold for loans to be no greater than 6.0x total leverage, which matches the Interagency Guidance on Leveraged Lending issued in 2013. Therefore, no loans originated by AP for BA have greater than 6.0x total leverage at underwriting. Second, it should be noted that AP typically invests in middle market loans which typically have a lower leverage profile than that of broadly syndicated loans. In fact, AP’s average leverage profile for new originations has been consistently lower than the market average for both senior and total leverage.

Lastly, AP focuses on what it considers the key risks and mitigants during its underwriting, as well as analyzing various sensitization analyses to demonstrate hypothetical downside performance. In line with the Interagency Guidance on Leveraged Lending, BA requires that all members make their own underwriting and credit decision before participating in a loan.

3. “Alongside these developments, standards and terms on business debt have continued to deteriorate. Although recent data from the Senior Loan Officer Opinion Survey on Bank Lending Practices indicate little change in lending standards for commercial and industrial (C&I) loans, banks had been easing these standards over much of the past two years. The risks associated with leveraged loans have also intensified, as a greater proportion are to borrowers with lower credit ratings and already high levels of debt. In addition, loan agreements contain fewer financial maintenance covenants, which effectively reduce the incentive to monitor obligors and the ability to influence their behavior. The Moody’s Loan Covenant Quality Indicator suggests that the overall strictness of loan covenants is near its weakest level since the index began in 2012, and the fraction of so-called cov-lite leveraged loans (leveraged loans with no financial maintenance covenants) has risen substantially since the crisis.”[6]

While most new leveraged loan originations are now covenant-lite (85% for the broadly syndicated market and 65% for the middle market), all loans originated by AP for BA must have at least one covenant per the BA RAC. As a side note, there is limited data to show that loans without covenants recover less than loans with covenants. To monitor performance against covenants, AP actively monitors all loans in the BancAlliance portfolio and re-risk rates the loans on a quarterly basis. AP also has an independent loan review conducted by Strategic Risk Associates to corroborate AP’s risk rating. Lastly, AP’s credit committee evaluates diluting mechanisms, such as “free and clear” incremental facilities and other credit weakening terms.

AP issued a bulletin in August 2018 which addressed the Moody’s study on covenants.

4. “A slowdown in economic activity could result in an increase in default rates, which would lead to elevated credit losses at financial institutions holding corporate debt, especially given the reduced amount of covenant protection on leveraged loans. Higher default rates and losses could also materialize through a sharp repricing of credit risk, which would lead to an increased debt service burden on firms with financing needs.”[7]

An economic slowdown would indeed increase default rates and lead to elevated credit losses. While it is logical that recovery rates may be lower due to the prevalence of covenant-lite structures, at this point in time, there is limited historical data to support that claim.

The average historical default rate for leveraged loans is typically ~2.5% – 3.0% with the current rate at 1.59% as of April 2019[8]. The Standard & Poor’s Leveraged Commentary & Data (“LCD”) Default Survey recently asked portfolio managers their predictions on the loan default rate at the end of 2020. The consensus estimate was 2.58% by then, a slightly more bullish read this time around, with managers reining in the forecast from 2.79% at the December reading.

Some market participants and observers believe that the leveraged loan market was created and has evolved to mitigate systemic risk and prevent contagion to the credit markets. A portfolio manager for PIMCO recently published in article in which she states “Given loan market dynamics, size, and scope, the diversity of the end holders, and the change in the leverage employed across the system, it is difficult for us to envision a scenario in which the leveraged loan market caused the next financial crisis.”[9]

The Report seems to echo these claims and mentions:

“On the whole, banks appear well positioned to deal with these exposures. The annual stress-test exercises stress a range of participating banks’ direct and indirect exposures to shocks from the business sector. The tests require that participating banks have sufficient capital to withstand material losses on these exposures and continue lending. In addition, banks’ internal liquidity stress tests and the Liquidity Coverage Ratio requirement incorporate protections against draws on credit lines. With regard to leveraged lending, banks have improved their management of the associated risks—reflecting, in part, the 2013 interagency guidance on leveraged lending—even as underwriting standards have deteriorated over the past decade. Moreover, large banks have improved their management of syndication pipelines.”

To mitigate risk on an individual bank level, AP encourages a detailed leveraged lending policy that clearly explains the rationale for engaging in a program to provide further diversification, as well as strict criteria governing portfolio size, portfolio diversification, individual loan size, governing credit characteristics, and a monitoring framework.

Conclusion

The growth of the leveraged loan market and the increase in investor appetite has certainly given rise to more aggressive credit terms. It is no surprise that this growth has received attention from the federal banking agencies.

The Federal Reserve Financial Stability Report and Regulators have pointed out that this growth combined with increased leverage and deteriorating underwriting standards give rise for concern. However, they also comment that the current default environment is at an all-time low and that the risk is appropriately distributed in the market to avoid systemic risk.

AP continues to believe that the leveraged loan market, and

in particular, the middle market, offers meaningful opportunity to earn an

attractive risk adjusted return and build a diversified portfolio. To mitigate risks in the market, both

perceived and real, AP will continue to underwrite to the RAC set by BA and

continue to actively monitor the BA portfolio.

[1] Financial Stability Report. May 2019. Board of Governors of the Federal Reserve System

[2] MarketWatch. Fed’s Quarles says leveraged loan buildup isn’t a replay of subprime crisis. May 7, 2019. https://www.marketwatch.com/story/feds-quarles-says-leveraged-loan-buildup-isnt-a-replay-of-subprime-crisis-2019-05-07

[3] Financial Stability Report. Pgs. 18- 19. May 2019. Board of Governors of the Federal Reserve System

[4] Beth MacLean. PIMCO. US Leveraged Loan Market: Plenty of Risk, But Not Systemic. February 2019.

[5] Financial Stability Report. Pgs. 19- 20. May 2019. Board of Governors of the Federal Reserve System

[6] Financial Stability Report. Pg. 22. May 2019. Board of Governors of the Federal Reserve System

[7] Financial Stability Report. Pg. 24. May 2019. Board of Governors of the Federal Reserve System

[8] Standard & Poor’s Leveraged Commentary & Data (LCD). April’s loan default rate of 1.01% (by principal amount) remains near multi-year lows. May 1, 2019.

[9] Beth MacLean. PIMCO. US Leveraged Loan Market: Plenty of Risk, But Not Systemic. February 2019.