Update On LIBOR – Part 2

Update on LIBOR – Part 2

Update

On April 25, 2019, the Alternative Reference Rates Committee (ARRC) released proposed fallback language that could be incorporated into syndicated loan credit agreements during initial origination or by way of amendment before the cessation of LIBOR occurs.

This article gives an overview of the situation, a summary of the ARRC’s recommendations for proposed fallback language and discusses what the BancAlliance bank network is seeing and its recommendations.

Background Refresh

In 2014, as a result of a rate-setting scandal, the Board of Governors of the Federal Reserve System and the Federal Reserve Bank of New York embarked on a program to secure an alternate reference rate for LIBOR. It ultimately selected the Secured Overnight Financing Rate (SOFR) as a suitable replacement for LIBOR and began publishing SOFR overnight rates a year ago. The Board then commissioned the Alternative Reference Rates Committee (ARRC) to develop fallback language for existing and future floating rate note (FRNs) transactions, among other financial structures, that are initially tied to LIBOR, in anticipation of the end of LIBOR in 2021[1].

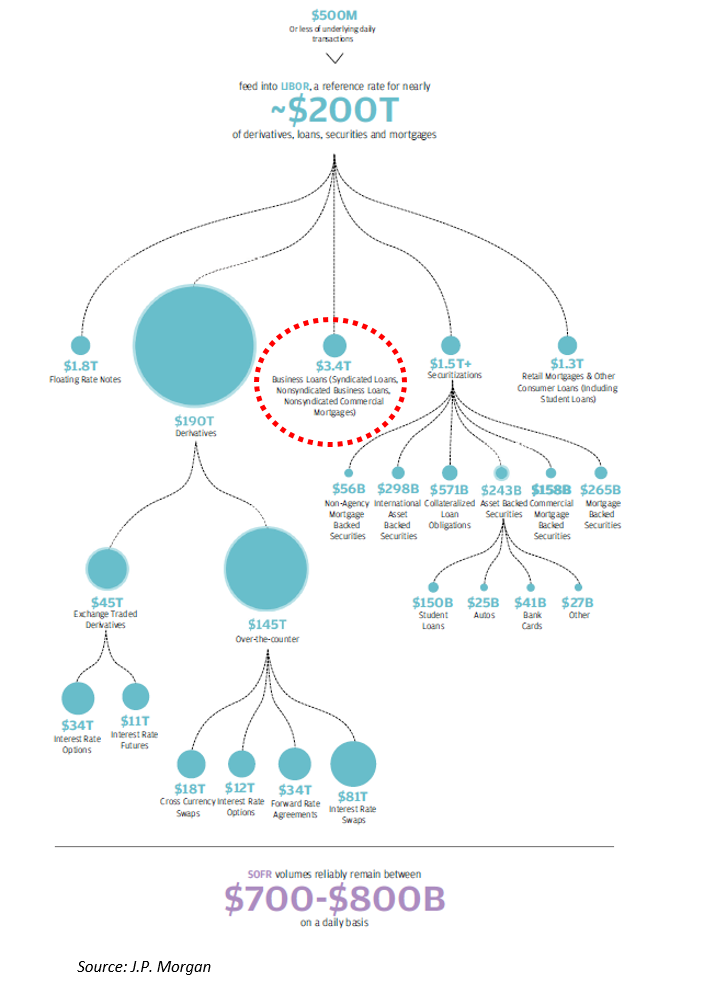

The graphic above gives an illustration of all the transactions in the ~$200 Trillion debt market tied to LIBOR[2]. It should be noted that syndicated loans only make up ~$3.4T, or ~1.7% of the overall debt market (which includes derivatives, loans, securities and mortgages).

SOFR vs LIBOR

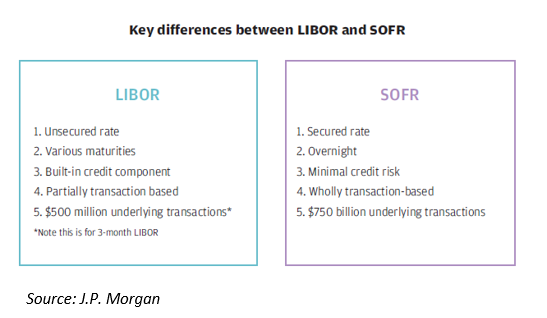

The ARRC selected SOFR as its new benchmark reference rate to replace LIBOR. Moving from LIBOR to SOFR requires various moving pieces to converge. For example, fresh debt linked to the new reference rate must be issued, futures and swaps markets need to grow, and lawyers have to develop more robust contractual language not only for new activities, but also to address legacy issues for existing contracts tied to LIBOR.

Furthermore, because SOFR is an overnight rate, the market needs to model a term structure – also known as a yield curve – with different maturities to reflect expectations about where interest rates will be in the future. The ARRC is currently tackling how to build a forward-looking SOFR term rate as part of its transition plan and aims to publish indicative rates using derivatives.

Several additional key differences are noted below[3]:

Need for Clarity in Fallback Language

The ARRC was initially tasked with identifying an alternative reference rate for LIBOR. After selecting SOFR, the ARRC was reconstituted in 2018 with an expanded membership, including regulators, trade associations, exchanges and other intermediaries, and buy side and sell side market participants, to oversee the implementation of the Paced Transition Plan and coordinate with cash and derivatives markets as they address the risk that LIBOR may not exist beyond 2021. This includes both minimizing the potential disruption associated with LIBOR going away and supporting a voluntary transition away from LIBOR.[4]

Fallback language is needed because outside of the derivatives world, fallback language is frequently inconsistent, particularly across products and institutions. The definition of LIBOR, the trigger for the fallbacks, and the fallbacks themselves vary significantly, even within the same product sets. Additionally, existing contractual fallback language was typically originally intended to address a temporary unavailability of LIBOR (i.e. glitch affecting the designated screen page or a temporary market disruption, not its permanent discontinuation. Until recently, such language was rarely written to address explicitly the possibility of the permanent discontinuance of LIBOR. As a result, legacy fallback language may result in unintended economic consequences and/or potential litigation[5].

ARRC Recommendations for Fallback Language

The ARRC recommends two sets of fallback language for new originations of LIBOR-referenced U.S. dollar-denominated syndicated loans. The syndicated loan fallback provisions try to balance several goals of the ARRC – flexibility and clarity[6].

- “Hardwired Approach” – This approach uses clear and observable triggers and successor rates with spread adjustments that are subject to some flexibility to fall back to an amendment if the designated successor rates and adjustments are not available at the time a trigger event becomes effective.

- “Amendment Approach” – This approach is meant to offer standard language which provides specificity with respect to the fallback trigger events, explicitly includes an adjustment to be applied to the successor rate, if necessary, to make the successor rate more comparable to LIBOR, and includes an objection right for “Required Lenders”. In the Amendment Approach language, all decisions about the successor rate and adjustment will be made in the future.

The ARRC’s proposal is then broken down into four distinct segments and briefly summarized below[7]:

- The Trigger Events causing the interest rate under to switch from LIBOR to the fallback benchmark: This includes defining a Permanent Cessation event vs a Precessation Trigger event (“Trigger Event”) and what exactly must occur to determine each of these Trigger Events. For example, Trigger events could include a public statement or publication by the administrator of a benchmark that the benchmark rate no longer exists. It could also include a public statement or publication by a regulatory supervisor announcing that the Benchmark is no longer representative.

- The Benchmark Rate that will then replace LIBOR: If a Trigger Event occurs, the ARRC recommends a new “Benchmark Replacement” that will be substituted for LIBOR on that date (the Benchmark Replacement Date). If the Benchmark Transition Event does not impact all tenors (e.g., one-month LIBOR, three-month LIBOR, etc.) of LIBOR and an interpolated LIBOR rate can be calculated for an impacted tenor based on unaffected LIBOR tenors, such interpolated rate will be the Benchmark Replacement for the applicable impacted tenor. If such interpolation is not possible, the ARRC recommendations including a waterfall of methodologies for determining the Benchmark Replacement.

- The applicable adjustments to Benchmark Replacements, if any, that will have to be made in the selected fallback benchmark: As there are differences between LIBOR and SOFR, there may need to be adjustments between the spreads to make them more comparable. As of the date of ARRC’s release, the methodologies for rate adjustments have not been developed, although it is clearly a goal of ARRC to develop them. Therefore, the ARRC has proposed a fallback waterfall similar to the structure used in the Benchmark Replacement

- Certain Benchmark replacement conforming changes: In addition to the Benchmark Replacement Adjustments, the issuer is entitled to make technical, administrative or operational changes in the underlying documents that the issuer decides may be appropriate to reflect the adoption of a Benchmark Replacement, provided that it does so in a manner substantially consistent with market practice. These changes might include changes in the definition of Interest Period, the timing and frequency of determining rates and making interest payments, addressing terms unique to LIBOR-based loans such as illegality, increased costs and breakage fees, and other administrative matters.

What BancAlliance[8] (BA) is Seeing

All of BA’s legacy loans have some form of standard fallback language. Most of the older vintage loans typically give the Agent discretion to choose a suitable replacement rate if LIBOR is not available. More recent credit agreements started to give negative consent to Required Lenders (i.e. lenders making up > 50% of the lending group) if they disagree of the replacement rate selected by the Agent. Credit Agreements also often contain an alternative base rate definition that could serve as a backup in the event LIBOR is not available and there is not a defined fallback mechanism for replacing LIBOR.

More recently, BA has seen new originations for larger broadly syndicated loans contain the new amendment style language in Credit Agreements although, older Credit Agreements have yet to be amended or updated with the new language. Due to the relative size of the $3 Trillion syndicated loan market compared to the overall size of the ~$200 Trillion debt market that uses LIBOR, there has not been a movement to rapidly transition to SOFR until SOFR’s use becomes more widely adopted in the broader market and other pertinent issues are resolved (i.e. ability to create a forward curve). Given that the transition isn’t expected to occur until the end of 2021, it would appear that most of the market is still in the “wait and see” mode.

The Fed is actively encouraging wider adoption of SOFR to accelerate acceptance. Most recently, Randal Quarles, the Federal Reserve vice chairman in charge of financial regulation, urged companies and financial institutions on Monday to speed up their preparations for a looming interest-rate shift. However, despite these calls by industry regulators, SOFR continues to be less widely embraced than LIBOR. While the amount of debt linked to SOFR surpassed $100 billion last month, roughly eight times that amount of Libor-linked notes have been sold, according to data from Wells Fargo & Co.[9] There hav been limited, if any, syndicated loans originated using SOFR as a pricing index. However, there was recently reported a private issuance of a syndicated loan with pricing tied to the SOFR index.

BA will continue to monitor the implementation of fallback language within newly originated Credit Agreements as well as its existing portfolio.

Recommendations

As the market continues to prepare for LIBOR’s eventual exit, there are several steps that BA recommends with respect to syndicated loans to prepare for this transition:

- Quantify, document and monitor exposure to Credit Agreements in your portfolio with LIBOR based pricing.

- Ensure you are familiar with the current LIBOR fallback language in the individual Credit Agreements within your portfolio.

- Be mindful should any amendments occur to your existing portfolio occur as SOFR’s acceptance grows in the marketplace and may lead to changes in legacy loans.

- Continue to observe new originations to see how fallback language is being implemented and any other structural changes with regards to LIBOR.

- Review ARRC pronouncements and market related current events to ensure you and your institution are up to speed on the latest news and changes with respect to LIBOR.

[1] Holland & Knight Alert. Douglas I. Youngman and Barbara M. Yadley. Summary of ARRC’s Libor Fallback Proposal for Floating Rate Notes. May 23, 2019.

[2] JP Morgan. Leaving LIBOR: A Landmark Transition. January 2019.

[3] JP Morgan. Leaving LIBOR: A Landmark Transition. January 2019.

[4] ARRC Recommendations Regarding More Robust Fallback Language for New Originations of LIBOR Syndicated Loans. April 25, 2019.

[5] Oliver Wyman and Davis Polk. LIBOR Fallbacks in Focus: A Lesson on Unintended Consequences. 2018.

[6] ARRC Recommendations Regarding More Robust Fallback Language for New Originations of LIBOR Syndicated Loans. April 25, 2019.

[7] Holland & Knight Alert. Douglas I. Youngman and Barbara M. Yadley. Summary of ARRC’s Libor Fallback Proposal for Floating Rate Notes. May 23, 2019.

[8] BancAlliance is a community bank network made up of over 250 banks across the United States. BancAlliance is managed by Alliance Partners, LLC, a wholly owned subsidiary of Congressional Bank.

[9] Daniel Kruger. The Wall Street Journal. Fed Official Urges Firms to Speed Shift From LIBOR. June 3, 2019.